February 16, 2025/

No Comments

Business and Financial News, Expert Opinions & International News How DeepSeek AI is Disrupting the...

31.10.2020

Ghana’s social media and political space have been pre-occupied with the ‘age-old’ debate on public debt and which of the two political parties, namely the NPP and NDC, left the biggest hole in the country’s public finances. Stoking up the debate is a recently published (October 2020) IMF Sub Saharan Africa Regional Economic Outlook report in which the Fund is forecasting that the country’s debt-to-gross domestic product (GDP) will reach 76.7% by the end of 2020 – potentially the highest since 2002.

The release comes ahead of the December 2020 presidential elections which is expected to be closely fought by the two parties. Some have indicated that Ghana is going back to the erstwhile Highly Indebted Poor Country (HIPC) status, but the IMF and other official releases have debunked this.

So, what is the history of Ghana’s public debt and fiscal deficits since 2001? In the next section, I create various charts based on publicly available data to show the underlying trends and provide some contextual commentary.

Public debt, deficit statistics and growth rates under NPP 1 (2001-2008), NDC 2 (2009-2016) and NPP 2 (2017-2019 and 2020 forecast)

The IMF defines gross debt as follows: “gross debt consists of all liabilities that require payment or payments of interest and/or principal by the debtor to the creditor at a date or dates in the future. This includes debt liabilities in the form of special drawing rights (SDRs), currency and deposits, debt securities, loans, insurance, pensions and standardized guarantee schemes, and other accounts payable” (Government Finance Statistics Manual, 2001, paragraph 7.110).

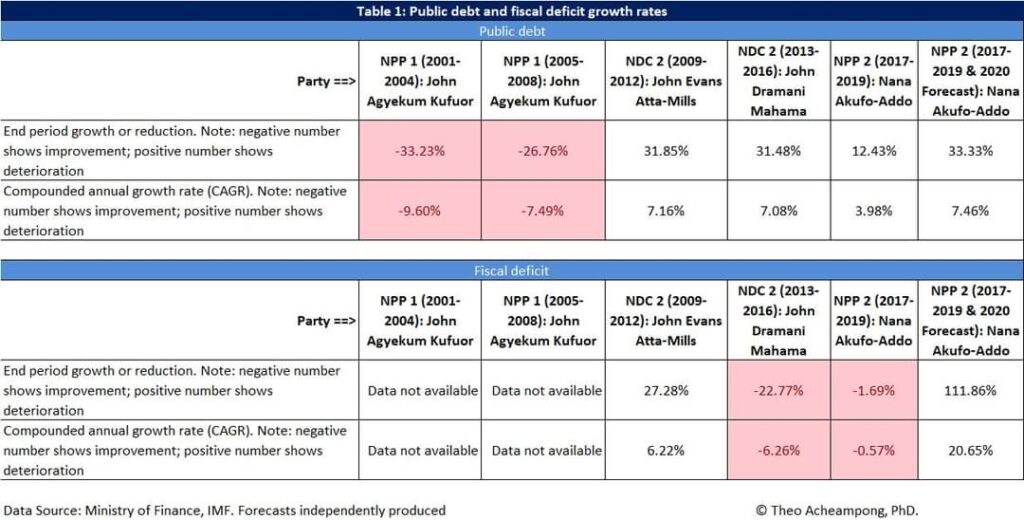

The rate of growth or reduction means the frequency at which debt is added or subtracted annually. Computationally, it is taking the final number at the end of the party or president’s tenure divided by the beginning number and subtracting one from it.

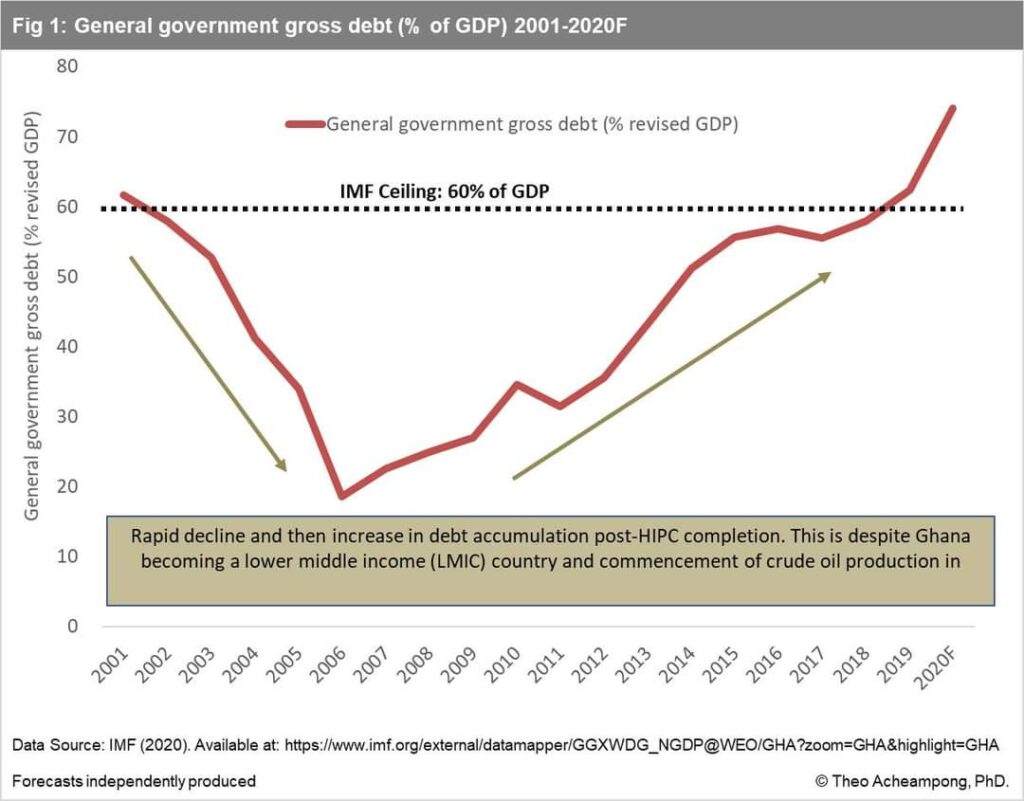

As Figure 1 and Table 1 show, Ghana’s gross public debt reduced by 33 percentage points between 2001 and 2004, and a further 27 percentage points reduction between 2005 and 2008 during the second term of President Kufuor. This massive reduction was due to the country signing on to the Heavily Indebted Poor Countries (HIPC) initiative in 2001 and Multilateral Debt Relief Initiative (MDRI) in 2005 – all under former President John Agyekum Kufuor. HIPC and MDRI came with a significant reduction in Ghana’s multilateral and bilateral debts owed to the likes of the IMF, World Bank and African Development Bank, among others.

However, debt accumulation began to pick up in 2006 – when we recorded our lowest public debt of 18.6% of GDP – and has been on the ascendency to date (Figure 1). The NDC under the late President John-Evans Atta mills increased the public debt by 32 percentage points between 2009 and 2012 while President John Dramani Mahama also increased it by another 32 percentage points at the end of his tenure in 2016, despite the rebasing of Ghana’s GDP.

In September 2018, the Ghana Statistical Service (GSS) rebased its economic calculations from the base year of 2006 to 2013. The GSS had earlier changed the base year for Ghana’s GDP calculation from 1993 to 2006. This rebasing shrunk Ghana’s debt-to-GDP ratios from 2013 onwards. For example, Ghana’s GDP was worth 26 times more from the original USD42 billion to USD 53 billion in 2017. The base year is very important in determining the size of a country’s GDP and other metrics such as the public debt and overall debt sustainability analysis (DSA) which relies on it. Likewise, the rebasing meant that Ghana’s hitherto 72.5% debt-to-GDP at the end of 2016 had magically shrunk to 56.8% of the rebased GDP in 2016.

These rebased figures created the expectations of extra fiscal space being available because after all, 57% is much better than 73%. No? The NPP, likewise, on winning the 2016 elections increased the public debt by 12 percentage points from 55.5% to 62.4% of rebased GDP between 2017 and 2019 (Table 1). My assessment of the fiscal data indicates that Ghana’s public debt will increase by 33% representing 74% debt to GDP by the end of 2020 (Table 1). This includes additional COVID-19-related expenditures and revenue downturns.

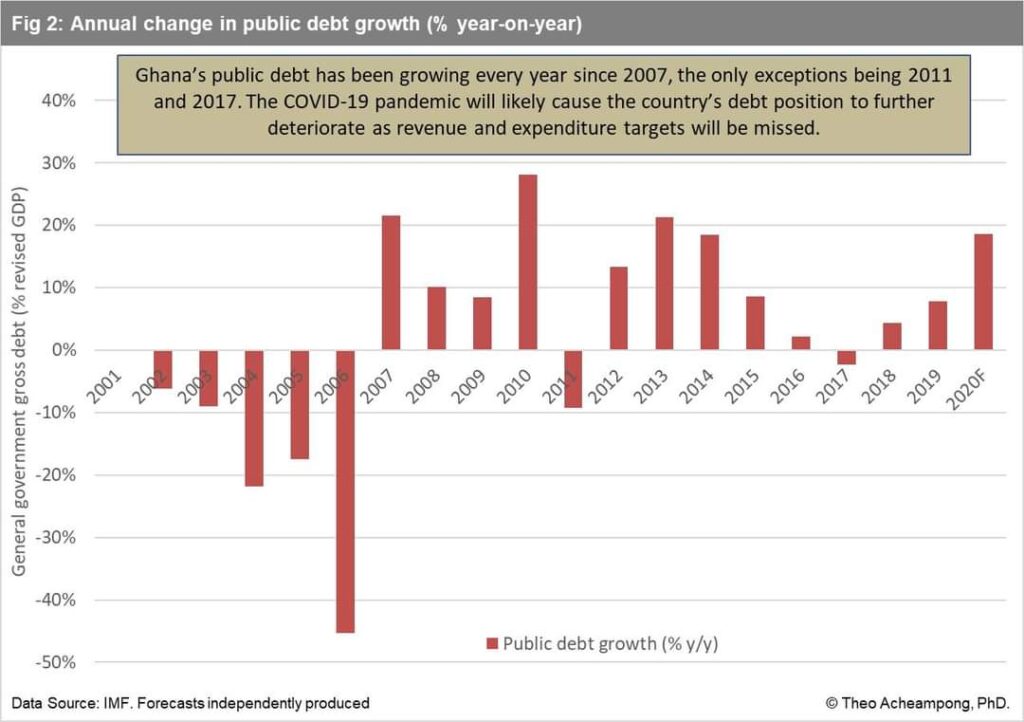

Ghana’s public debt accumulation since 2017 has been driven primarily by the twin – financial and energy sector debts. Government has spent GHS21 billion (USD 3.7 billion or 5.6% of 2018 GDP) in cleaning up the financial sector (universal, savings and loans, microfinance) which commenced in August 2017. The COVID-19 pandemic will likely cause the country’s debt position to deteriorate further as revenue and expenditure targets are missed. The reality is that Ghana’s public debt has been growing every year since 2007, the only exceptions being 2011 and 2017 (see Figure 2).

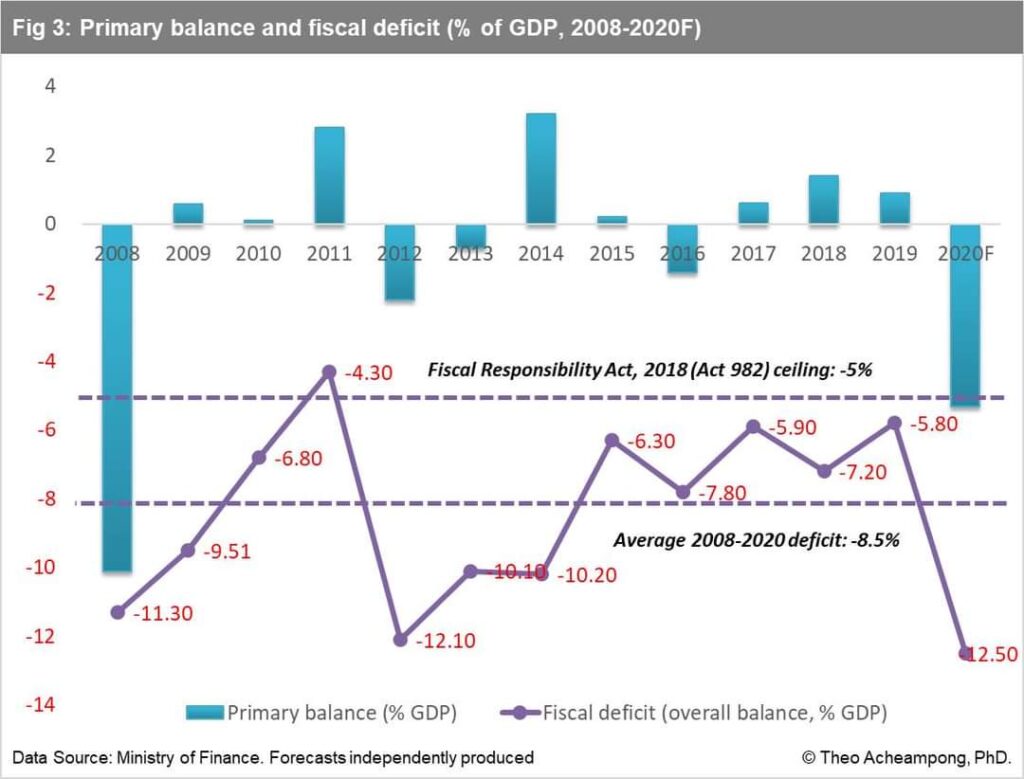

Also, the fiscal deficit since 2010 has never been below 5% of GDP despite a positive primary balance in some years (See Figure 3). The fiscal deficit is unlikely to reduce significantly over the next four years (2021-2024) due to the constrained revenue envelope and structural rigidities in the budget manifesting in extra expenditures, including debt servicing costs.

Ghana has had to resort to external or commercial financing of its budget since it became a lower-middle-income country (LMIC) in 2011 with loss of access to relatively cheaper concessional loans. Thus, commercial debt continues to be the largest source (41%) of external debt liabilities due to significant Eurobonds portfolio. Eurobonds have been a regular financing mechanism for Ghana; the country has borrowed USD12 billion in Eurobonds from 2007 to 2020. Also, about 70% of the external debt is dollar-denominated with significant impacts for the cedi. For example, the amortisation of 2012 and 2014 Eurobonds are expected in 2024 and 2026, respectively.

While the government reported deficits (overall balance including discrepancy) of 3.9% and 4.8% of GDP for 2018 and 2019, it is important to note that this excludes the cost of the financial sector clean-up. Essentially, the government, through the Ministry of Finance, was treating these costs as below the line or one-offs. Hence, the total deficit or overall balance (cash, discrepancy) including the financial sector clean-up cost) was much higher at 7.2% of GDP in 2017 and 5.8% of GDP in 2018 respectively, as indicated in the various fiscal outturn reports, which are publicly available on the finance ministry’s website.

In conclusion, except for the Kufuor administration (2001-2008) which managed to bring down Ghana’s public debt levels significantly, both the Atta Mills (2009-2012), Mahama (2013-2016) and Akufo-Addo (2017-2020) administrations have added to the public debt in similar amounts.

The writer is an economist and political risk analyst.

Business and Financial News, Expert Opinions & International News How DeepSeek AI is Disrupting the...

Expert Opinions & Politics and Governance The Re-Election of President Mahama: Implications and Future Prospects...

Expert Opinions & Politics and Governance “From Tradition to Transformation: Uncovering the Dynamic Innovations of...

Expert Opinions Africa’s Prosperity and Population Growth: A Statistical and Business Case Perspective E. N....

Business and Financial News, Expert Opinions & Politics and Governance Ghana’s decades of darkness: Finance...

Business and Financial News & Expert Opinions Taxation vs. Debt: Is Ghana making the Right...

©2024. Tunani Africa – Ghana. All Rights Reserved | Designed by XCreativs Technologies